This chain of blocks provides an immutable record that enhances trust, transparency, and easy audit trails. Payment in cryptocurrencies like Bitcoin is also faster and more cost-effective. However, the technology is not without its drawbacks. Scalability remains a significant challenge, as does the energy cost associated with mining processes. Businesses looking to invest in blockchain must also navigate complex government regulations.

A Comparative Analysis of Strengths and Weaknesses in the Top 12 Aspects

| Aspect | Advantages | Disadvantages |

|---|---|---|

| Decentralization | – No single point of failure – Enhanced security – Reduced risk of fraud | – Vulnerable to 51% attacks if one entity gains majority control |

| Transparency | – Public, verifiable ledgers – Audit trails for transactions – Increased trust | – Once data is added, it’s difficult to modify |

| Immutability | – Permanent record of transactions – Accountability – Reduced risk of tampering | – Hard forks required for data modification – Older data is almost impossible to change |

| Efficiency | – Faster transactions – Lower transaction costs – No intermediaries | – High energy consumption in Proof of Work systems – Scalability issues |

| Security | – Cryptographic algorithms – Multi-signature transactions – Identity protection | – Loss of private key means loss of assets – Vulnerable to quantum computing (theoretically) |

| Accessibility | – Open-source platforms – Global reach – Financial inclusion | – Requires internet access – Technical know-how needed |

| Cost | – Reduced transaction fees – No third-party fees – Microtransactions possible | – Initial setup cost for private blockchains – Transaction fees in public blockchains |

| Data Storage | – Distributed storage enhances data integrity – Data is more secure | – Blockchain ledgers can grow very large – Storage concerns for individual nodes |

| Auditability | – Every transaction is recorded – Easier for compliance and auditing | – Public ledgers might expose sensitive data |

| Interoperability | – Blockchain bridges for cross-chain transactions – Tokenization of assets | – Not all blockchains are interoperable – Complexity in cross-chain transactions |

| Regulation | – Smart contracts for automated compliance – Transparency aids regulatory oversight | – Regulatory uncertainty – Potential for misuse in illegal activities |

| Innovation | – Constantly evolving ecosystem – New solutions like Layer 2 for scalability | – Rapid changes may leave some users behind – Risk of obsolescence |

At a time when digital security and data management are at the forefront of personal and professional concerns, the word “blockchain” often appears as a potential solution. If you find yourself in this situation, you’re probably looking for a clear and balanced understanding of what blockchain technology actually offers in terms of advantages and disadvantages. You may be wondering, “Is blockchain right for my business?”; “What are the real applications of this decentralized technology?”; or even, “Is it worth the financial investment and media hype?”

This article aims to answer these pressing questions by taking a deep dive into the specific pros and cons of blockchain technology. We’ll examine its potential impact on a variety of sectors, including its role in financial transactions, supply chain management and digital identity verification. With a balanced perspective, we’ll help you navigate the complexities and potential trade-offs of this disruptive technology. Stay tuned for all you need to know about the promises and limitations of blockchain, and how it fits your particular needs.

The Transformative Advantages of Blockchain Technology

Decentralization, Security, and More Decentralization:

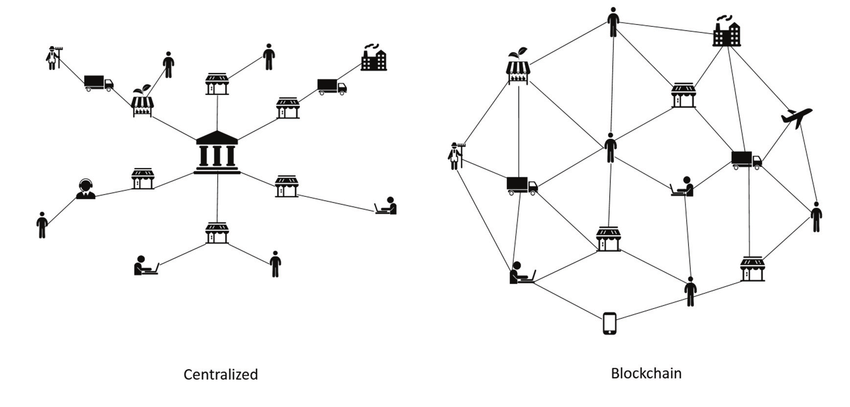

The Cornerstone of Autonomy and Data Security Decentralization stands as a transformative feature that fundamentally distinguishes the blockchain from traditional systems. In centralized models, a single entity or group of related entities hold the authoritative power to control, validate, and secure all activities. This concentration of power not only creates a single point of failure but also introduces multiple layers of intermediaries, each adding its own set of complexities and costs. In contrast, a decentralized approach operates on a peer-to-peer network, distributing the control and validation across multiple participants.

Blockchain architecture inherently eliminates the need for a central authority, thereby reducing the risk of system-wide failures and potential data manipulations.

The absence of intermediaries in a decentralized setup brings about a host of benefits, chief among them being reduced transaction costs and enhanced speed and efficiency. For instance, in financial ecosystems, the peer-to-peer nature of the network allows for direct transactions between parties, cutting out banks and payment processors who would otherwise take a cut for their services. Similarly, in real estate transactions, property records can be securely and transparently transferred without the need for brokers or legal representatives, thereby streamlining the process and reducing associated costs. This level of autonomy not only democratizes the transaction process but also opens up possibilities for innovation and new business models that were previously unimaginable under centralized systems.

Real-World Application:

Decentralized Finance (DeFi) platforms are a prime example. These platforms allow users to borrow, lend, or trade assets directly with each other, bypassing traditional financial institutions. This not only democratizes financial services but also significantly reduces transaction costs.

Security:

A Fortified Digital Fortress with Immutable Records The security protocols integrated into the blockchain are a paradigm shift from conventional methods, setting a new standard for digital safety. In traditional systems, the centralized nature often makes them vulnerable to a range of security threats, including data breaches and unauthorized access. In contrast, this blockchain employs a multi-layered security approach that begins with transaction verification. Each transaction is rigorously scrutinized and must be collectively agreed upon by participants in the network before it can be recorded. This consensus mechanism ensures that fraudulent or erroneous transactions are easily identified and rejected by the network, adding an additional layer of security.

Once a transaction gains the necessary approval, it undergoes encryption and is linked to the preceding transaction in the distributed ledger technology, forming a chain. This chained relationship between transactions ensures that any attempt to alter a single transaction would necessitate changes to all subsequent transactions, a feat that would require enormous computational power and is thus practically unfeasible. Furthermore, the ledger is not stored in a single location but is distributed across multiple nodes or computers. This decentralization of data storage further fortifies the system against hacking attempts and fraudulent activities. Even if one node is compromised, the integrity of the entire system remains intact, thereby safeguarding the data stored within it.

Real-World Application:

Healthcare is one sector that could significantly benefit from blockchain’s robust security features. Patient records can be securely stored on a blockchain, providing both the patients and healthcare providers with a reliable and immutable history of medical treatments, thereby ensuring data integrity and reducing the risk of medical errors.

Transparency and Traceability:

An Unbroken Chain of Trust Another major advantage of blockchain technology is its transparency. Every transaction is recorded in the ledger and is publicly accessible to all participants. This level of openness serves as a tool for accountability, making it difficult for any entity to manipulate data to their advantage. While participants can remain anonymous or pseudonymous, their actions are entirely transparent, creating an environment of trust and integrity. This is especially useful in industries like supply chain management, where the transparency of a blockchain can provide a real-time, unbroken chain of trust from the manufacturer to the retailer.

Real-World Application

The food industry has begun utilizing blockchain technology to enhance transparency in supply chains. By recording the journey of food products from farm to store shelf, consumers can have greater confidence in the authenticity and safety of what they consume. Companies like IBM have developed blockchain-based solutions for food traceability that are already in use today.

Disruptive Potential Across Industries Blockchain’s ability to bring about decentralization, enhance security, and ensure transparency positions it as a disruptive force across a wide array of sectors. Beyond its applications in finance and supply chain management, blockchain holds the potential to revolutionize industries like healthcare, real estate, voting systems, and even intellectual property rights management. As the technology matures and adoption rates increase, it’s reasonable to expect a plethora of innovative applications that could reshape existing systems and create new paradigms of operation.

Reduced Transaction Costs: Efficiency at Its Best

The efficiency of the blockchain is most evident in its ability to significantly reduce transaction costs. Traditional systems often involve multiple intermediaries, each adding their layer of fees and time delays. However, the decentralized nature of this technology eliminates the need for these middlemen, thereby streamlining the transaction process. This not only speeds up transactions but also cuts down on the costs associated with them.

For example, in the realm of international money transfers, the traditional banking system can be slow and laden with fees. The blockchain enables real-time, cross-border transactions at a fraction of the cost, making it an efficient alternative for both individuals and businesses. The cost-saving aspect is not limited to financial transactions, it extends to various other sectors like real estate, legal processes, and supply chain management, where the absence of intermediaries translates to quicker processes and substantial cost reductions.

The Hurdles Ahead: Challenges and Limitations of Blockchain Technology

While blockchain technology offers transformative advantages, it’s essential to recognize its limitations and challenges. Here are some of the key obstacles that need to be addressed for blockchain to reach its full potential:

Scalability:

One of the major hurdles for blockchain is its scalability issue. As the number of transactions increases, the computational power required to process and validate these transactions also escalates, making it increasingly difficult to scale the network without compromising its speed and efficiency. Solutions like layer 2 protocols and sharding are being explored to address this concern, but these are still in developmental stages

Regulatory and Legal Barriers:

As a disruptive technology, blockchain often faces regulatory uncertainties and legal challenges. The absence of standardized regulations makes it difficult for industries to adopt blockchain technology fully. For instance, in the financial sector, the lack of clear guidelines on cryptocurrencies and decentralized platforms poses a significant hurdle for mass adoption.

Initial Costs and Complexity: Implementing blockchain technology requires a substantial initial investment, both in terms of hardware and expertise. Additionally, the complex nature of blockchain makes it less accessible for average users, limiting its adoption to those with the technical know-how.

Interoperability:

As more blockchain platforms emerge, the lack of interoperability between different blockchains poses a challenge. Projects like Polkadot and Cosmos are aiming to solve this problem by allowing different blockchains to interact with each other, but these are still in their nascent stages

Real-World Application: Challenges in Healthcare In the context of healthcare, the sensitivity of patient data and the need for compliance with regulations like the Health Insurance Portability and Accountability Act (HIPAA) in the United States create additional complexities for blockchain adoption. Questions surrounding data ownership, access control, and the interoperability between existing systems and new blockchain-based solutions are yet to be fully addressed.

The Disadvantages of Blockchain Technology and Cryptocurrencies

Scalability Issues:

The scalability (the ability to scale) is one of the main challenges facing public blockchains like Bitcoin and Ethereum. Here are some of the issues and ongoing solutions:

- Transaction Throughput: For example, Bitcoin can only process around 7 transactions per second (tps), and Ethereum around 30 tps, which is significantly insufficient for global applications. For comparison, Visa can handle around 24,000 tps.

- Latency: The time required for a transaction to be confirmed can also be problematic, especially for applications requiring quick confirmations.

- Storage: The ever-growing size of the blockchain demands a lot of storage space, which can be a problem for full nodes.

Solutions for Scalability:

Layer 1 Solutions

- Protocol Optimization: Improvements at the protocol level itself, like changing the consensus algorithm, can increase the transaction throughput.

- Sharding: A technique that divides the network into multiple shards that can process transactions in parallel.

Layer 2 Solutions

- Payment Channels: For example, Bitcoin’s Lightning Network allows for nearly instantaneous transactions between parties off the main blockchain, with final settlements on the blockchain.

- Rollups: For Ethereum, solutions like Optimistic Rollups and zk-Rollups allow for bundling multiple transactions into a single one, thus reducing the load on the main blockchain.

Other Approaches

- Parallel Blockchains/Sidechains: Secondary blockchains can be created to offload certain transactions from the main blockchain.

- Data Fragmentation: Techniques like breaking files into smaller pieces can also help.

Each solution has its pros and cons in terms of security, decentralization, and complexity. Research is ongoing to find ways to make blockchains more scalable without compromising their security or decentralization.

Complexity Issues:

- High Energy Consumption: One of the most frequently cited issues with blockchain, particularly in proof-of-work systems like Bitcoin, is its high energy consumption. The computational power required for transaction verification and consensus can be as much as that of entire countries, leading to significant environmental concerns.

- Regulatory Challenges: The decentralized and borderless nature of blockchain technology makes it difficult to apply traditional legal frameworks, causing a lack of clarity in governance and compliance requirements.

Potential Solutions for Complexity:

Technological Solutions

- Transition to Proof-of-Stake (PoS) or other Consensus Algorithms: These algorithms typically consume less energy compared to Proof-of-Work (PoW) systems, thereby reducing the environmental impact.

- Optimized Transaction Processing: Algorithms and methods that require less computational power to verify transactions can reduce the energy footprint.

Regulatory Solutions

- Standardized Frameworks: Creation of universal regulatory guidelines that accommodate the unique aspects of blockchain technology can offer clarity in governance and compliance.

- Smart Contracts for Governance: Decentralized networks could use smart contracts to automatically enforce rules and regulations, minimizing the need for a centralized authority and making governance more transparent.

Other Approaches

- Renewable Energy: Encouraging the use of renewable energy sources for mining operations could mitigate the environmental impact.

- Regional Regulations: Countries could enact laws that either restrict or guide the energy consumption of blockchain operations within their jurisdictions.

Each of these solutions comes with its own set of challenges in terms of implementation, security, and global standardization. However, they offer a way forward for making blockchain technology less complex and more sustainable in both environmental and regulatory contexts.

Energy Consumption Issues:

- High Energy Usage: One of the most cited drawbacks of blockchain technology, especially in proof-of-work systems like Bitcoin, is its high energy consumption. The energy required for transaction verification and achieving consensus can rival that of entire countries.

- Environmental Concerns: The high energy consumption contributes to environmental degradation and raises questions about the long-term sustainability of such networks.

- Operational Costs: The high energy usage not only has environmental implications but also makes operating a blockchain network expensive, limiting its feasibility for smaller organizations and developing countries where energy costs are a significant concern.

Potential Solutions for Energy Consumption:

Technological Solutions

- Transition to Proof-of-Stake (PoS) or other Consensus Algorithms

- Optimized Transaction Verification

Economic Solutions

- Incentivizing Low-Energy Mining: Creating economic incentives for miners to use renewable energy or low-energy mining methods could help mitigate the environmental impact.

- Scaling Solutions: Implementing Layer 2 solutions like sidechains or rollups can reduce the transaction load on the main network, leading to less energy consumption for transaction verification.

Other Approaches

- Renewable Energy Sources: Encouraging or mandating the use of renewable energy for blockchain operations could mitigate some environmental concerns.

- Regional Energy Caps: Governments could impose energy consumption caps on blockchain operations, forcing them to adhere to local sustainability guidelines.

Storage Issues:

The Burden of Permanence Blockchain’s immutable nature means that data, once added, cannot be removed. Over time, this can lead to enormous data storage requirements, especially for blockchain networks that handle a high volume of transactions. The storage burden can become a logistical and financial challenge for nodes participating in the network, potentially leading to centralization as only large organizations can afford the storage costs.

This also raises concerns about data privacy and identity. Since the blockchain ledger is permanent and publicly accessible, any sensitive information accidentally or illicitly added to the blockchain becomes a permanent part of the public record, posing potential risks to individual privacy and data protection.

Storage Issues:

- Growing Storage Requirements: The immutable nature of blockchain means that data, once added, cannot be removed. This leads to ever-increasing data storage needs, especially for networks with high transaction volumes.

- Financial and Logistical Challenges: The need for significant storage can become a financial burden for nodes, potentially leading to centralization as only large organizations can afford the ongoing storage costs.

- Data Privacy Concerns: Because the blockchain ledger is permanent and publicly accessible, any sensitive information that is accidentally or illicitly added becomes a permanent public record, posing risks to individual privacy and data protection.

Potential Solutions for Storage Issues:

Technological Solutions

- Pruning: Some blockchain networks allow for “pruning” of older transaction records that are not needed for current transaction verification, reducing the storage requirements on full nodes.

- Sharding: Breaking the blockchain data into smaller pieces (shards) and distributing them across multiple nodes can alleviate the storage burden on individual nodes.

Governance Solutions

- Data Entry Guidelines: Implementing strict rules and smart contracts to regulate what kinds of data can be added to the blockchain can prevent the addition of unnecessary or sensitive information.

- Incentivized Storage: Offering financial rewards to nodes that take on greater storage responsibilities can help distribute the burden more equitably.

Other Approaches

- Off-Chain Storage: For certain types of data, especially large files, off-chain storage solutions can be implemented. In this scenario, only a cryptographic “pointer” to the data is stored on the blockchain.

- Zero-Knowledge Proofs for Privacy: Implementing cryptographic techniques like zero-knowledge proofs can enable verification of transactions without revealing the underlying data, offering a layer of privacy.

Issues Related to 51% Attacks:

- Manipulation of Transaction Verification: When a single entity gains control of the majority of a blockchain network’s computational power, they can manipulate the transaction verification process, allowing for activities like double-spending.

- Undermining Trust and Integrity: A successful 51% attack can severely damage the trust and integrity of the blockchain network, which could result in a loss of users and value.

- Particular Vulnerability of Smaller Networks: While large, well-established networks are less likely to suffer from a 51% attack due to the sheer amount of computational power required, smaller or newer blockchains are particularly vulnerable.

Potential Solutions for 51% Attacks:

Technological Solutions

- Alternate Consensus Mechanisms: Moving away from Proof-of-Work (PoW) to alternative consensus mechanisms like Proof-of-Stake (PoS) or Delegated Proof-of-Stake (DPoS) can make 51% attacks more difficult and costly.

- Adaptive Protocols: Some blockchain networks are exploring adaptive protocols that can dynamically adjust the requirements for achieving consensus, making it more difficult to execute a 51% attack.

Governance Solutions

- Node Incentivization: Encouraging a larger and more diverse set of nodes to participate in the network can make it more resistant to 51% attacks.

- Watchtowers and Monitoring: Implementing real-time monitoring systems that can detect unusual network behavior and trigger protective mechanisms.

Other Approaches

- Penalty Systems: Introducing penalties for malicious activities can serve as a deterrent for entities contemplating a 51% attack.

- Time-Locked Deposits: Requiring nodes to lock up a certain amount of assets for a specific period can act as a financial deterrent against launching an attack.

Challenges and Potential Solutions: A Comparative Table

| Aspect | Issues | Potential Solutions |

|---|---|---|

| Scalability | 1. Low transaction throughput 2. Latency 3. Storage | 1. Protocol Optimization 2. Sharding 3. Payment Channels 4. Rollups |

| Complexity | 1. High energy consumption 2. Regulatory challenges | 1. Switch to PoS 2. Optimized Transaction Processing 3. Standardized Regulatory Frameworks |

| Energy Consumption | 1. High energy usage 2. Environmental concerns 3. High operational costs | 1. Switch to PoS 2. Optimized Transaction Verification 3. Use of Renewable Energies |

| Storage Issues | 1. Growing storage requirements 2. Financial and logistical challenges 3. Data privacy concerns | 1. Pruning 2. Sharding 3. Data Entry Guidelines 4. Off-chain Storage |

| 51% Attacks | 1. Transaction verification manipulation 2. Loss of trust and integrity 3. Vulnerability of smaller networks | 1. Alternate Consensus Mechanisms 2. Adaptive Protocols 3. Node Incentivization 4. Penalty Systems |

Things to remember

Weighing up the pros and cons Blockchain technology has its share of pros and cons. Its transformative potential for improving transparency, trust and efficiency in a variety of sectors is undeniable. However, challenges such as scalability, regulatory uncertainty and high costs cannot be ignored.

Final thoughts on the impact of blockchain In conclusion, blockchain technology and crypto-currencies are at a pivotal point in their development. Their transformative potential is enormous, offering a new paradigm for conducting transactions, securing data and improving transparency. However, the road to mainstream adoption is fraught with pitfalls, requiring innovative solutions. The future is bright, but the road ahead is still under construction.